Pet Insurance

Policy Decoder

Upload your pet insurance policy PDF and get an accurate plain-English breakdown with coverage, exclusions, red flags and more.

Works on iPhone, Android & desktop

Analysing your policy…

Sniffing out what's covered…

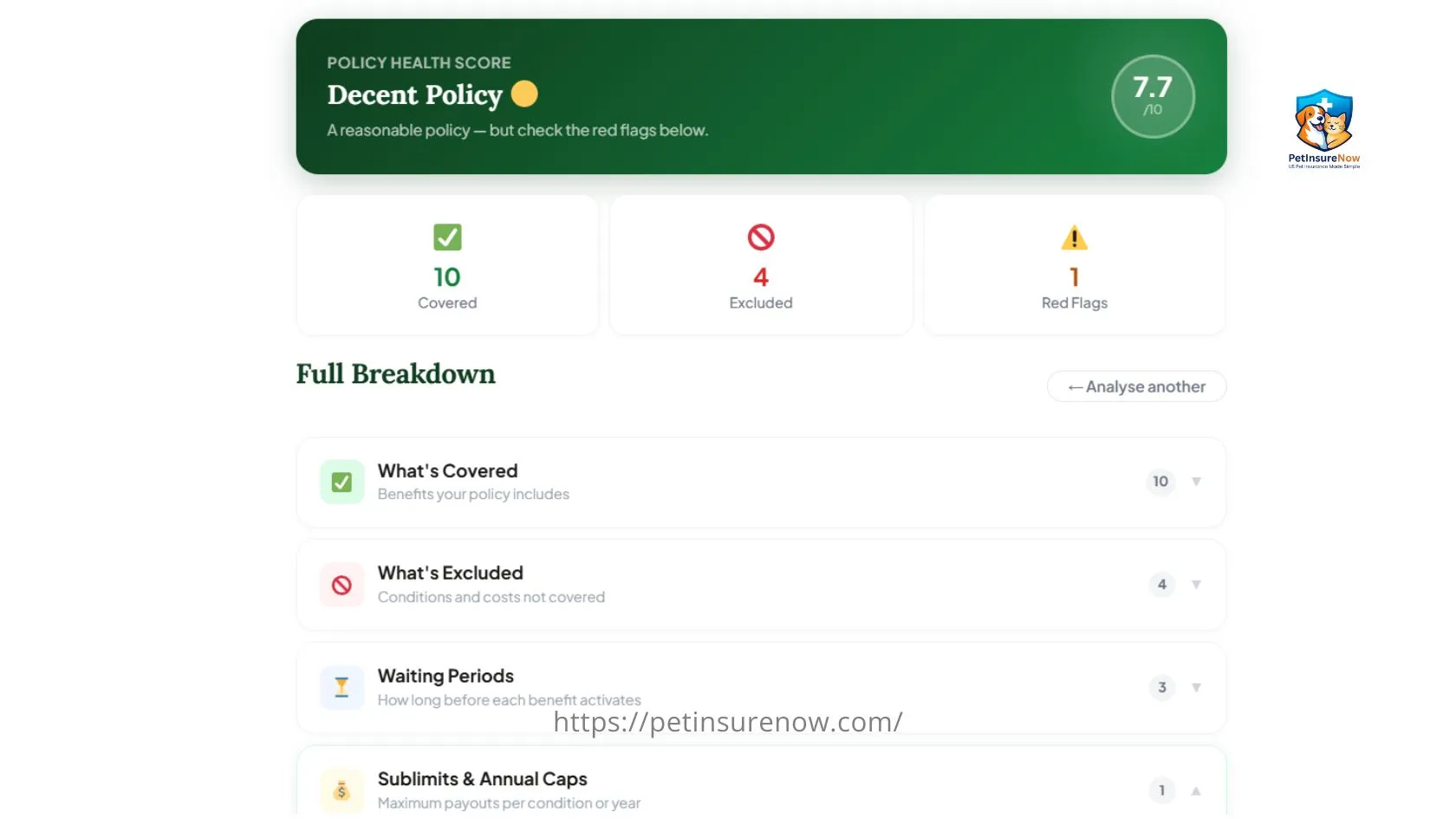

Full Breakdown

Before signing or renewing, ask your insurer these questions — the answers could save you thousands in denied claims:

Found something concerning?

Compare pet insurance plans and find one that truly protects your pet.

⚠️ This tool uses pattern-matching analysis and provides a plain-English summary for informational purposes only — not legal or financial advice. Results labelled "Typical" are industry averages, not confirmed policy details. Always read your full policy and contact your insurer directly with specific questions. PetInsureNow.com is not responsible for inaccuracies in this analysis.

What Is a Pet Insurance Policy Decoder?

A Pet Insurance Policy Decoder is a tool that reads the technical language in a pet insurance contract and converts it into plain-English that any pet owner can understand. Pet insurance policies are written by legal teams and are intentionally dense, they use terms like ‘bilateral conditions,’ ‘UCR pricing,’ ‘per-incident deductibles,’ and ‘contestability periods’ without explanation. Most pet owners sign these contracts without understanding the clauses that most commonly cause claim denials.

A Pet Policy Decoder does the hard work for you. It scans the policy text, identifies the critical clauses, and tells you in plain language: what you are getting, what you are not getting, and what you need to watch out for.

The PetInsureNow’s Pet Policy Decoder is specifically built for pet insurance policies, not for generic insurance, not life insurance, not car insurance. It understands pet-specific clauses like bilateral joint exclusions, breed-specific restrictions, orthopedic waiting periods, and hereditary condition coverage. No other free tool on the market offers this level of pet insurance specificity.

How to Use the Pet Policy Decoder, Step by Step

Using the decoder takes under two minutes. Here is the step-by-step process:

- Upload your policy PDF or paste text. Click the ‘Upload PDF’ tab and select your pet insurance policy document from your phone or computer (up to 10MB, text-based PDFs work best). Or click ‘Paste Text’ and copy any section directly from your policy.

- Click ‘Decode My Policy.’ The tool analyses your document instantly with no waiting, no account needed.

- Review your Policy Health Score. The decoder gives your policy a score out of 10, based on the number of red flags, exclusions, and concerning clauses detected.

- Read your colour-coded breakdown. Each section (covered, excluded, waiting periods, sublimits, red flags) is clearly organised so you can scan quickly or read in depth.

- Use the Questions Checklist. Before you call your insurer or sign anything, tick off the 10 most important questions from our built-in checklist.

- Get a free quote if needed. If your policy score is low or you find concerning clauses, use our comparison tool to find a better plan.

What the Decoder Analyses?

1. Coverage

Most pet insurance marketing focuses on what policies cover. Accidents. Illnesses. Emergencies. But coverage in the fine print is always narrower than the headline. The decoder identifies every specific covered item in your policy text: from cancer treatment and diagnostic tests to specialist consultations and alternative therapies. Understanding what is covered and at what rate is the first step in determining if you’re getting the coverage you need.

2. Exclusions

Exclusions are where most pet owners get surprised. Pet insurance policies typically exclude pre-existing conditions, cosmetic procedures, breeding-related costs, grooming, and experimental treatments. But the exclusions that catch most people off guard are the ones buried in complex language: bilateral condition clauses (if your dog injures one knee, the matching knee may be excluded forever), breed-specific restrictions, and ‘not medically necessary’ determinations. The decoder flags every exclusion it detects, with a plain-English explanation of what it means for your pet.

3. Waiting Periods

Pet insurance policies all come with waiting periods – a period after the policy is purchased in which some conditions won’t be covered. The standard waiting periods in US pet insurance are: 0 to 2 days for accidents, 14 days for illness, and 6 months for orthopedic conditions. This 6-month orthopedic waiting period is important: the most common and expensive dog injury is cruciate ligament tears, which average $5,000 to $7,000 to repair, and are excluded if they occur within 6 months of the policy start. The decoder extracts the exact waiting periods in your policy so you know exactly when your coverage actually begins.

4. Sublimits and Annual Caps

A pet insurance policy could have an annual limit of $10,000. But the policy contains sublimits – limits to particular conditions. For example, a policy might have a sublimit of $500 for specialist treatment, $1,000 for dental disease and $300 for alternative therapies per year. The sublimits greatly diminish the effective coverage of the policy. The decoder pulls out every amount of deductible, percentage co-pay, reimbursement percentage, annual limit, and sublimit it can from your policy.

5. Red Flags and Gotchas

Some clauses in pet insurance policies are not illegal, but they are genuinely harmful to policyholders who do not understand them. The decoder specifically flags: per-condition deductibles (charged separately for every new condition, not once per year), UCR pricing caps (reimbursement capped at regional ‘usual and customary’ rates rather than your actual vet bill), bilateral exclusions, and premium escalation language. These are the clauses that insurance brokers rarely explain, that policy documents bury in legalese, and that most pet owners only discover when a claim is rejected.

How to Spot Most Common Pet Insurance Red Flags

The decoder automatically detects these nine red flags. Understanding what they mean before you upload your policy makes your results even more actionable.

Red Flag 1: Per-Condition Deductible

When most people think of their pet insurance deductible, they assume it’s the same as health insurance – a deductible paid once a year, and then the insurance pays the rest. Per-condition deductibles are different: you pay a separate deductible every single time your pet develops a new condition. For a dog with allergies, a cruciate tear, and a skin infection in the same year, you could pay three separate deductibles. Over a pet’s lifetime, this can cost thousands more than an annual deductible policy.

Red Flag 2: Pre-Existing Condition Exclusion (Permanent)

The vast majority of pet insurance plans don’t cover pre-existing conditions. But it’s a critical term. Other insurers will exclude any condition your pet had any sign of before the policy started (even if it wasn’t diagnosed or treated, and is only noted in passing in older veterinary records). If your dog limped two years ago and it was noted in the vet records, you may not be able to claim for a bilateral (both sides) knee injury. Be sure to check with your insurer about how they define pre-existing conditions before purchasing.

Red Flag 3: Bilateral Exclusion Clause

A bilateral exclusion clause means that if your pet has a covered condition in one body part (their right knee, their left hip, their right eye) the same condition in the corresponding body part is excluded – even if it occurs years later and is unconnected. This is particularly common for dogs with cruciate ligament injuries (Golden Retrievers, Labradors) and hip dysplasia (German Shepherds, Rottweilers). It’s one of the most costly, but least understood, clauses in pet insurance.

Red Flag 4: UCR (Usual and Customary Rates) Pricing Cap

UCR caps mean your insurer will only reimburse the ‘usual and customary’ rate they consider appropriate for your location – not the amount the vet charges. Emergency and specialist veterinarians typically charge between 30 to 60 percent higher than the UCR. If your dog requires emergency surgery that costs $4,000 and the UCR rate for that surgery in your area is $2,500, you will be reimbursed for $2,500 – not $4,000. This can be a huge difference for complicated surgeries.

Red Flag 5: Annual Premium Escalation

Pet insurance premiums increase every year as your pet ages. This is expected. What is less expected is the rate of increase. Some insurers raise premiums by 15 to 40 percent per year after claims. A policy that costs $50 per month when your dog is 2 years old could cost $120 to $180 per month by the time they are 7. If a policy contains language about ‘annual review’ or ‘rate adjustment,’ understand the implications before you commit.

Red Flag 6: Orthopedic Waiting Periods (6 Months)

The average waiting period for illness in pet insurance is 14 days. But orthopedic injuries (which include the most costly injuries) can have a 6 month wait. A torn cruciate ligament (equivalent to your ACL) is $5,000 to $8,000 per knee. If your dog tears a cruciate within 6 months of your policy start date, you receive nothing. This is the most expensive single gap in most pet insurance policies.

Red Flag 7: Exam Fees Excluded

Every vet visit starts with a consultation or exam fee, typically $60 to $150. Many pet insurance policies do not cover this fee, even when everything else about the visit is covered. For a pet with a chronic condition requiring quarterly visits, that is $240 to $600 per year in uncovered costs. Some premium insurers (like Pumpkin and Figo) include exam fees. If yours does not, budget for it separately.

Red Flag 8: Hidden Sublimits

A policy’s advertised annual limit is not the amount you can claim for any specific condition. Sublimits cap payouts for specific categories at amounts far below the headline limit. A $15,000 annual limit policy might have: $500 sublimit for specialist care, $1,000 for dental illness, $500 for alternative therapy, and $2,000 for cancer treatment. Knowing the sublimits is the only way to understand the true value of your policy.

Red Flag 9: Breed-Specific Exclusions

Some insurers place restrictions on coverage for specific breeds or groups of breeds, particularly brachycephalic breeds (French Bulldogs, English Bulldogs, Pugs) and large breeds prone to orthopedic issues (German Shepherds, Great Danes, St. Bernards). Coverage for hereditary conditions common in your pet’s breed may be limited, excluded, or available only as an expensive add-on. Always check breed-specific terms before buying.

Calculate Your Pet Insurance Cost

Answer a few quick questions — get an instant estimate for your pet’s coverage

Frequently Asked Questions

What is a pet insurance policy decoder?

A pet insurance policy decoder is a free tool that analyses your pet insurance policy document, translating the legalese into simple language. It highlights coverage, exclusions, waiting periods, sublimits, and hidden red flags such as bilateral exclusions and UCR caps on pricing – the clauses most often used to deny pet insurance claims.

Is there a free tool to understand my pet insurance policy?

Yes. The PetInsureNow’s Pet Insurance Policy Decoder is a 100% free tool that analyses any pet insurance policy. You can upload a PDF (maximum file size 10MB) or copy and paste any clause, and get an instant plain-English summary of coverages, exclusions, waiting periods, annual limits and other red flags. No registration or email address needed.

What are the most common pet insurance exclusions?

The most common pet insurance exclusions are: pre-existing conditions (anything your pet showed signs of before the policy started), cosmetic or elective procedures, breeding and pregnancy costs, routine dental cleaning, grooming, food and supplements, and experimental treatments. Some policies also exclude exam fees and specific breeds. Always read the exclusion section carefully before purchasing.

What is a bilateral exclusion in pet insurance?

A bilateral exclusion clause in a pet insurance policy means that if your pet suffers from a covered condition on one side of its body (such as the left knee or hip), the same type of condition on the opposite side of the body is never covered – even if it happens years later and for a completely different reason. It’s most common in dogs with cruciate ligament injuries and hip dysplasia.

What is UCR pricing in pet insurance and why does it matter?

Usual, Customary, and Reasonable (UCR) is a price cap that caps reimbursements at the regional average of vet fees, rather than the exact fee charged. If your veterinarian prices above this average (such as specialists and emergency clinics), you must pay the excess yourself after reimbursement. UCR caps can significantly impact the actual cost of your pet insurance.

What is the difference between a per-condition deductible and an annual deductible in pet insurance?

An annual deductible is paid once per policy year, regardless of how many conditions your pet develops. A per-condition deductible is charged separately each time your pet develops a new condition. For pets with multiple health issues, per-condition deductibles can cost significantly more. Annual deductible policies are generally more favourable for pets with chronic or recurring conditions.

How long are waiting periods in pet insurance?

Standard pet insurance waiting periods in the US are: 0 to 2 days for accidents, 14 days for illness, and 6 months for orthopedic conditions (such as cruciate ligament tears and hip dysplasia). Some policies also have waiting periods for cancer, dental conditions, and specific hereditary conditions. Coverage for any condition that occurs during the waiting period is denied.

What questions should I ask my pet insurer before buying?

Before buying pet insurance, ask: (1) Is the deductible annual or per-condition? (2) Are hereditary conditions in my pet’s breed covered? (3) Does reimbursement apply before or after the deductible? (4) Are exam fees included? (5) How do you define pre-existing conditions? (6) Is there a bilateral condition clause? (7) What are the sublimits for cancer, orthopaedic surgery, and specialists? (8) What happens to my premium after a claim?

Can I upload my pet insurance PDF to understand it better?

Yes. The PetInsureNow Policy Decoder will analyse pet insurance PDFs up to 10MB in size. It finds all of the text in the PDF and then scans it for coverage, exclusions, waiting periods, sublimits and other issues. It’s best to use text-based PDFs (the type you get from your insurer). The text may not extract properly from scanned-in or image-based PDFs (in this case, paste the text).

What is a policy health score in pet insurance?

A policy health score rates your pet insurance policy out of 10 based on the number of concerning exclusions, red flags, and restrictive clauses detected in your policy document. A score of 8 to 10 indicates a comprehensive policy with few red flags. A score below 5 suggests multiple concerning clauses that could significantly limit your real-world coverage and should prompt you to compare alternative plans.

Why does my pet insurance policy have so many exclusions?

Exclusions are necessary in pet insurance for the insurer to control risk and keep premiums low for the majority of customers. Some exclusions (pre-existing conditions, elective surgerys, grooming) are standard. But other exclusions – such as bilateral clauses, UCR limits, and per-condition deductibles – are used to restrict payouts for major claims. Understanding every exclusion in your specific policy is critical before you need to make a claim.

How is PetInsureNow's Policy Decoder different from other insurance decoders?

Most policy decoders are built for generic human insurance (life, health, auto). PetInsureNow’s decoder is built exclusively for pet insurance. It detects pet-specific clauses including bilateral joint exclusions, orthopedic waiting periods, breed-specific restrictions, and hereditary condition coverage. It also includes a Policy Health Score, integrated questions for your insurer and no rate limits – all of which are missing from other decoders.